Verbal VOE for Mortgage: Process, Compliance, and Turnaround

Mortgage verbal VOE is a pre-closing employment check that helps lenders confirm a borrower is still employed before the note date. This article explains the process, documentation and compliance requirements, common failure points, and how to evaluate providers based on turnaround time, employer outreach, and audit-ready records.

Verbal VOE for Mortgage: Process, Compliance, and Turnaround

A loan file can be fully underwritten, conditions cleared, and closing scheduled for tomorrow morning. Then a verbal verification of employment fails to come back in time, and the closing slips. The borrower is frustrated. The loan officer is fielding calls. The ops team is chasing an HR department that closes at 3 PM Pacific.

Verbal VOE is one of the last steps in the mortgage production cycle, and it carries disproportionate risk relative to its apparent simplicity. It is a phone call, yes, but operationally it functions as a timing and documentation control that sits on the critical path to funding. When it works, nobody notices. When it breaks down, the closing date moves.

This article covers when verbal VOE is required, what a compliant record looks like, where the process commonly fails, and how to evaluate whether to handle it internally or through a third-party provider.

What is verbal VOE in mortgage lending?

Verbal verification of employment is a phone-based confirmation that a borrower is currently employed (or self-employed) at the time of the call. It is distinct from a written VOE, which is a formal letter or form completed by the employer, and from automated verification through database services like The Work Number.

The purpose is narrow: confirm that the borrower still holds the job that supports the income used to qualify for the loan. Verbal VOE does not typically re-verify income amounts, pay rates, or job tenure in the same detail as a written verification. It is a status check, timed close to closing, designed to catch employment changes that occurred after initial underwriting.

For mortgage operations teams, the key distinction is that verbal VOE must happen inside a defined window before the note date. That timing requirement turns a simple phone call into a scheduling and documentation problem.

When lenders need verbal VOE before closing

Agency guidelines create the clearest timing requirements. Fannie Mae's Selling Guide indicates that verbal verification of employment for employment income must be obtained within 10 business days prior to the note date. Freddie Mac references a similar pre-closing verification window in related guide materials.

Those 10 business days sound generous until you account for weekends, holidays, employer HR hours, and the reality that many closings are scheduled with short lead times. A loan cleared to close on a Monday may need the verbal VOE completed the prior week, which means the outreach attempt needs to start days earlier to allow for callbacks and escalation.

Individual lenders and investors may layer additional overlays on top of agency guidance. Some require verbal VOE within 5 business days of the note date, or within a certain number of days of funding rather than the note date. Operations teams should map their specific investor requirements rather than assuming a single standard applies across all products.

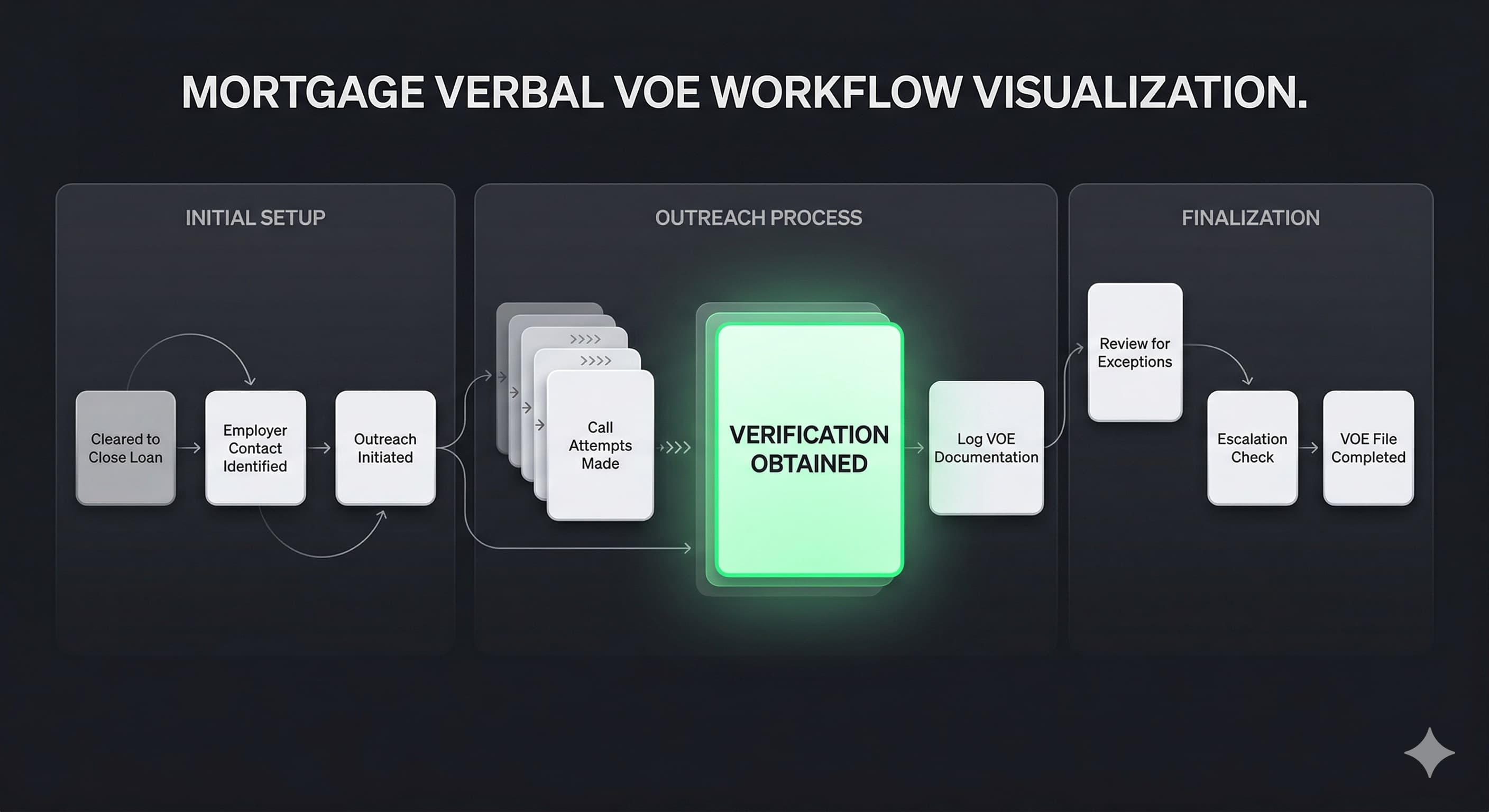

The mortgage verbal VOE process step by step

The workflow generally follows a predictable sequence, though execution varies by lender size and staffing model.

Trigger. The verbal VOE is ordered when the loan reaches clear-to-close or a similar milestone, with the closing date confirmed. Some lenders initiate the order earlier to build in buffer time, especially for borrowers employed by organizations known to be slow in responding.

Employer contact identification. The person completing the verification needs a valid phone number for the borrower's employer, specifically for HR, payroll, or a supervisor authorized to confirm employment. The phone number source matters for compliance purposes; using an independently verified number (from the employer's website or a third-party directory) is stronger than relying solely on a number the borrower provided.

Outreach and confirmation. The verifier calls the employer and confirms the borrower's current employment status. If the first attempt fails (line busy, voicemail, HR unavailable), the verifier follows up and documents each attempt.

Documentation. The outcome is recorded on a standardized form with fields covering who was contacted, when, and what was confirmed. If employment could not be verified, that outcome is documented too.

Escalation. When repeated attempts fail, the verifier notifies the lender so the team can decide whether to delay closing, try alternative verification methods, or request the borrower's help in facilitating contact.

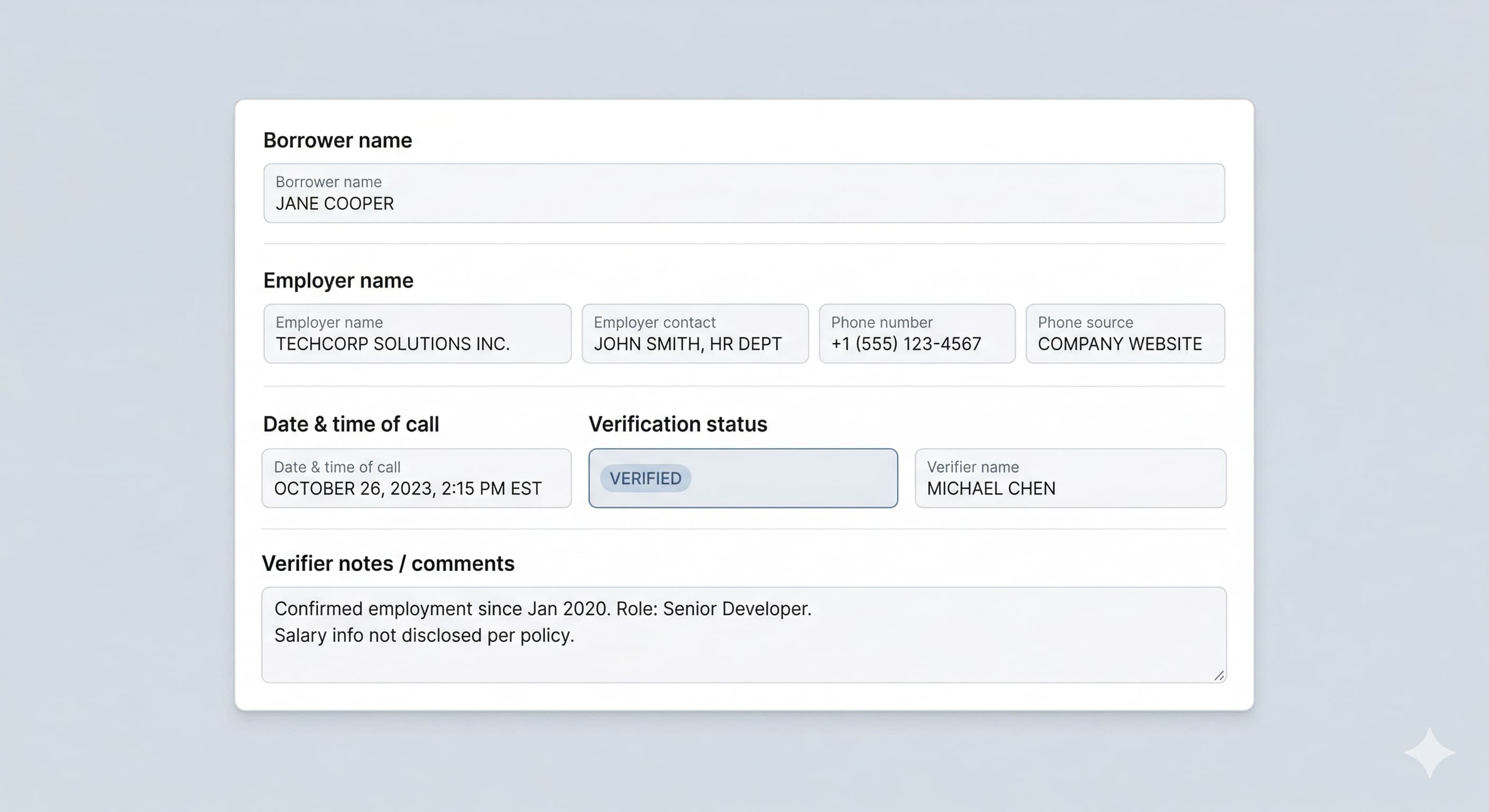

What a compliant verbal VOE record should include

Freddie Mac materials indicate the mortgage file must include Form 90, Verbal Verification of Employment, or a similar written document. The record should be structured enough to survive file review months or years after closing.

Core fields that agency and lender requirements often call for include:

- Borrower name

- Employer name

- Employer contact name or department

- Phone number used for the call

- Source used to obtain the phone number (employer website, third-party directory, borrower-provided, etc.)

- Date and time of the call

- Employment status confirmed (active, terminated, leave of absence, etc.)

- Name or identifier of the person who completed the verification

- Unable-to-verify outcome and reason, if applicable

The phone number sourcing field deserves attention. Documenting how the employer's number was obtained supports the credibility of the verification. A number pulled from an independent source is more defensible in QC review than one taken directly from the borrower without validation.

If the borrower's employment could not be confirmed, the record should clearly state the outcome and the steps taken. An "unable to verify" result with three documented call attempts and a voicemail log is a stronger file artifact than a blank field.

Compliance and audit trail requirements

Verbal VOE documentation is not just for the underwriter reviewing the file before closing. It also needs to hold up in post-close QC, investor audits, and internal reviews conducted months later.

Fannie Mae's quality control guidance supports the need for standardized, reviewable processes and retained records across mortgage production workflows. Verbal VOE fits within that framework as one of many operational controls that must be documented consistently. A QC reviewer pulling a random sample of closed loans should be able to confirm that the verbal VOE was completed within the required timeframe, with proper documentation, for every applicable file.

Separately, mortgage underwriting operates in a regulated environment where documentation quality affects defensibility. CFPB Regulation B, while not a verbal VOE rule, reinforces the broader principle that credit decisions require retained records and consistent processes. If an employment verification issue contributes to a loan decision, the file should contain clear evidence of what was checked, when, and what was found.

The practical takeaway for operations leaders: a verbal VOE provider or internal process that delivers fast completions but inconsistent documentation creates latent QC risk. Speed without a clean audit trail is not a net gain.

Why turnaround time matters so much

The 10-business-day window from Fannie Mae guidance is the outer boundary, not a comfortable cushion. In practice, the effective window is often shorter because of how closings are scheduled.

Consider a common scenario: a borrower's closing is set for Friday. The loan is cleared to close on Tuesday. The verbal VOE order goes out Tuesday afternoon. The employer's HR department operates Monday through Thursday, 8 AM to 4 PM Central. If the first call attempt on Wednesday goes to voicemail, the verifier has one more business day (Thursday) to reach HR before the employer's office closes for the week. A missed Thursday call could mean the Friday closing slips.

Same-day and next-business-day turnaround on verbal VOE completions matters because the pre-close window is not forgiving. Delays compound when employer contact data is stale, HR teams are understaffed, or the borrower works for a large organization with centralized employment verification lines that have long hold times. Turnaround is a real operational constraint, not a marketing differentiator.

Common failure points in mortgage verbal VOE

Most verbal VOE failures trace back to a few recurring problems.

Unresponsive HR departments. Some employers only confirm employment through written requests, refuse phone verifications, or route all inquiries through third-party verification services. Large employers increasingly use automated systems that do not accept inbound phone calls for employment confirmation.

Bad or outdated contact data. The phone number on file may be disconnected, may reach a general switchboard rather than HR, or may connect to a location where the borrower no longer works. Without an independent source for the employer's phone number, the verifier may waste attempts on the wrong line.

Inconsistent internal workflows. When verbal VOE is handled by whoever on the team is available, documentation standards drift. One processor may record thorough notes; another may write "confirmed employed" on a sticky note. That inconsistency creates QC findings.

Timing misalignment. If the verbal VOE order is placed too late, even a single failed call attempt can push the verification outside the required window. Operations teams that treat verbal VOE as a last-minute checkbox rather than a scheduled task tend to experience more closing delays.

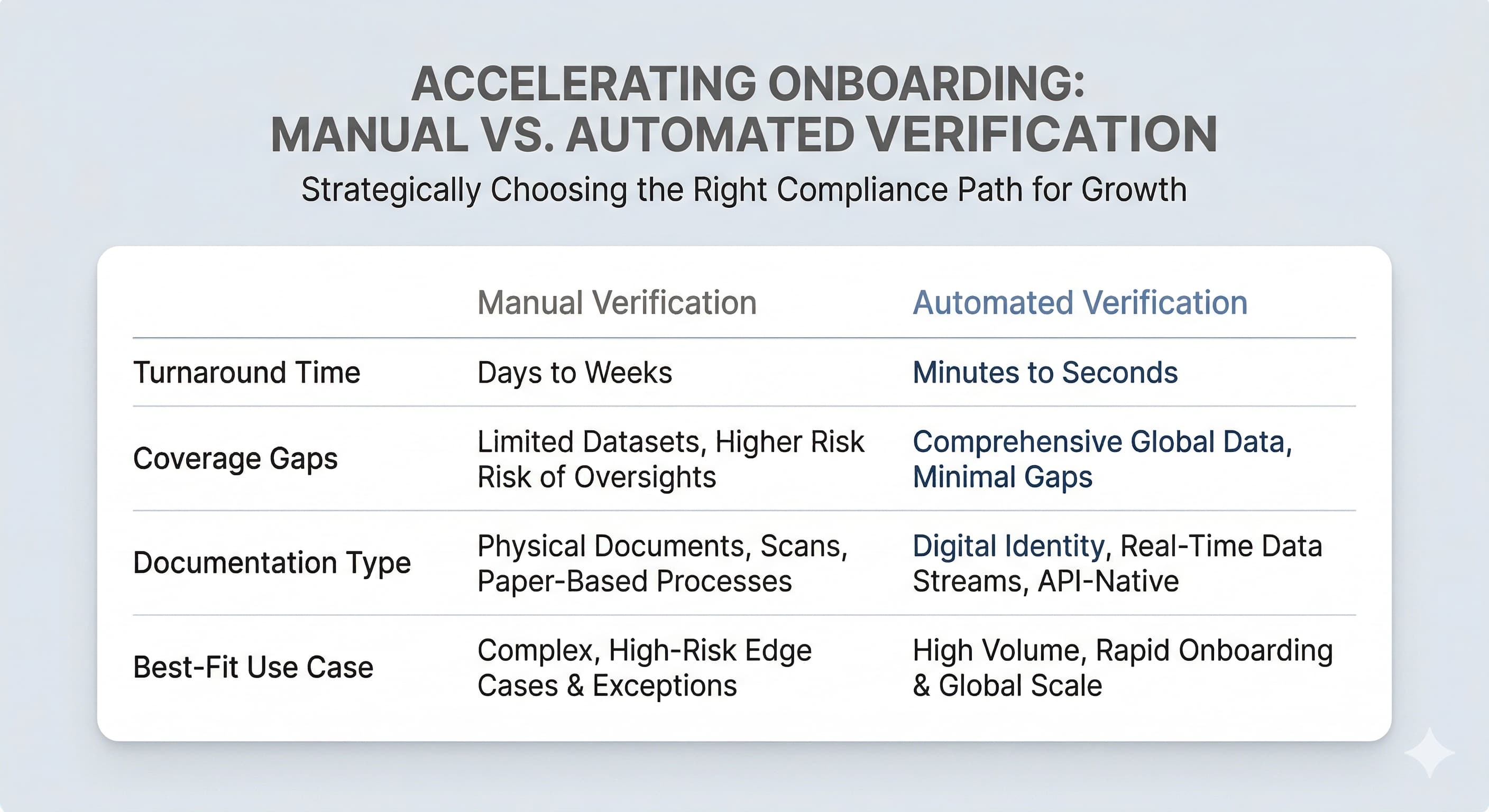

Manual vs automated employment verification

Automated employment verification services, such as database-driven platforms that pull records from payroll providers, can return employment confirmation in minutes. When the borrower's employer participates in one of these databases, automated verification is faster and produces a standardized report.

Manual verbal VOE is still needed in several common situations. The borrower's employer may not participate in any automated database. The automated record may be stale (reflecting last payroll run, not current employment status as of today). Some investors or lender overlays may require a phone-based verification in addition to an automated check, particularly when the closing date is very close.

The practical reality for most lenders is that automated verification handles a portion of the pipeline cleanly, and manual verbal VOE covers the rest. The split varies by borrower demographics, employer size, and geographic mix. Operations teams that rely solely on automated sources will still encounter files that require a phone call, and those files tend to surface at the worst possible time, right before closing.

What lenders should look for in a verbal VOE provider

Vendor evaluation for verbal VOE services should focus on four areas.

Turnaround time with documentation. The relevant metric is time to a completed, file-ready record, not just time to first call attempt. Ask how the provider handles employer non-response and how many attempts are standard before escalation.

Employer reach and contact validation. Providers that maintain or access independent employer directories can source phone numbers without relying on borrower-provided data. That sourcing step supports compliance and reduces wasted call attempts.

Documentation quality and format. The returned record should contain all fields needed for investor compliance and QC review, including the fields referenced in Freddie Mac's Form 90 guidance. Records should be timestamped and formatted for easy file integration, whether that means PDF, XML, or direct LOS upload.

Escalation discipline. When the first call fails, what happens next? A strong provider has a defined escalation protocol: multiple call attempts at different times, alternative contact methods, and a clear unable-to-verify process with documentation. Providers that simply report "unable to reach" after one voicemail do not solve the operational problem.

A useful question during vendor evaluation: ask how the provider handles employers that refuse phone verifications or require written requests. The answer reveals whether the vendor has real experience with the full range of employer response patterns or is only staffed for easy completions.

Key objections buyers raise

"We can handle verbal VOE in-house." Many lenders do. The question is whether internal staff can maintain consistent documentation standards, make timely follow-up calls during peak volume periods, and cover employer time zones without gaps. In-house calling works well at lower volumes with dedicated staff. It tends to break down when volume spikes or staff are pulled to other tasks.

"Same-day turnaround seems unrealistic." Same-day completion depends on employer reachability, not just the provider's effort. A reasonable expectation is same-day completion for employers that are reachable during business hours, with next-business-day completion for cases requiring follow-up. Any provider guaranteeing 100% same-day completion for all files is overpromising.

"What about compliance risk with a third party?" Using a vendor does not eliminate the lender's compliance obligation. The lender remains responsible for ensuring the verbal VOE was completed within the required window, that the documentation meets investor standards, and that records are retained. Vendor selection should include a review of the provider's documentation format and process controls, not just pricing.

"Is it worth the cost for something we can do with a phone?" The cost comparison should include the fully loaded expense of internal staff time, the risk of inconsistent documentation creating QC findings, and the cost of delayed closings when internal calling falls behind. For lenders with moderate to high volume, the math often favors a specialized provider, but lower-volume shops with disciplined processes may do fine in-house.

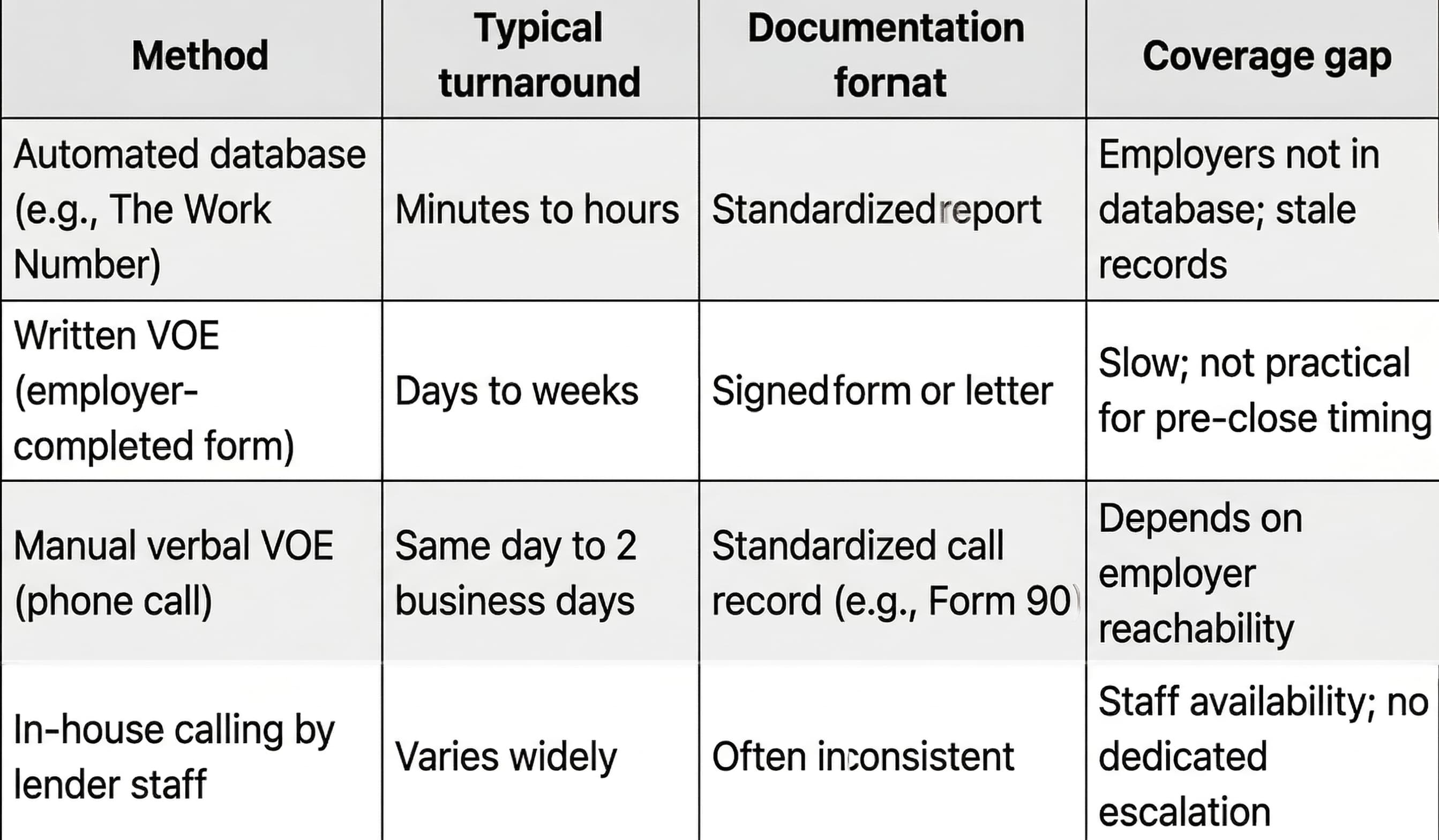

Comparison: verbal VOE, written VOE, automated verification, and in-house calling

Verbal VOE (outsourced). Best suited for pre-closing employment confirmation when the timeline is tight and documentation standards must be consistent across a high volume of files. Strengths are speed, standardized records, and dedicated follow-up. The tradeoff is cost and reliance on a third party.

Written VOE. Provides more detailed employment and income information than a verbal check, but turnaround is typically measured in days or weeks. Not practical as a pre-closing control when the window is 10 business days or fewer and the closing date is approaching.

Automated database verification. Fastest option when the employer participates. Produces a standardized report. The gap is coverage: employers not in the database require a fallback method, and automated records may not reflect employment status as of today.

In-house calling. Gives the lender direct control over the process. Works well when volume is manageable and staff are trained on documentation standards. Breaks down during volume spikes, staff turnover, or when callers lack dedicated time for follow-up and escalation.

Frequently asked questions

Does every mortgage loan require verbal VOE before closing?Agency and lender requirements vary. Fannie Mae guidance indicates verbal VOE is required for employment income within 10 business days of the note date. Other investors may have different rules or waive the requirement in specific circumstances. Check your investor guidelines rather than assuming a universal rule.

What happens if the employer cannot be reached before closing?The verification record should document the attempts made and the unable-to-verify outcome. Most lenders have escalation procedures, which may include having the borrower facilitate contact, trying alternative methods, or delaying closing until verification is complete. An undocumented gap is worse than a documented unable-to-verify result.

Can automated employment verification replace verbal VOE?In some cases, yes. Some lender and investor guidelines accept automated verification records as a substitute for phone-based verbal VOE when certain conditions are met. However, not all employers are covered by automated databases, and some investors still require a phone-based check close to the note date. Confirm with your specific investor guidelines.

What is Freddie Mac Form 90?Form 90 is Freddie Mac's standardized form for documenting a verbal verification of employment. It captures fields like borrower name, employer name, contact information, phone number source, date and time, and employment status. Lenders can use Form 90 or a similar written document that captures equivalent information.

Conclusion

Verbal VOE for mortgage is a timing and documentation control that sits on the critical path between clear-to-close and funding. The phone call itself is straightforward. The operational challenge is completing it within a narrow pre-close window, documenting it in a format that satisfies investor and QC requirements, and having a reliable escalation path when the employer is hard to reach.

Operations leaders evaluating their verbal VOE process, whether in-house or through a provider, should focus on three things: turnaround time measured to completed documentation (not just first attempt), record quality that meets agency standards like those reflected in Freddie Mac's Form 90, and a consistent process that holds up in post-close review. Getting the call done fast is necessary. Getting it done fast with a clean audit trail is what keeps files out of QC findings.

Related Posts

Employment Verification Outsourcing: A Guide for Lean HR Teams

Calling HR Departments for Employment Verifications

Verbal VOE for Tenant Screening: Speed, Process, and Documentation

Ready to get started?

Major CRAs trust us to handle the verifications no one enjoys — faster, cheaper, and fully documented. See how!