Argyle vs. Truework vs. The Work Number vs. Superunit: Employment Verification Compared

Equifax raised The Work Number's prices in January 2026. Here's how Argyle, Truework, The Work Number, and Superunit compare on coverage, pricing, turnaround time, and use case fit — and which one wins when databases return no result.

Argyle vs. Truework vs. The Work Number vs. Superunit: Employment Verification Compared 2026

Equifax raised prices on The Work Number effective January 1, 2026. For background screening companies, mortgage lenders, and tenant screeners who depend on TWN for employment verification, that price increase turned a routine budget line into an active vendor evaluation. Reports that previously cost $69.75 now cost more, and some use cases have historically run $130.69 per report.

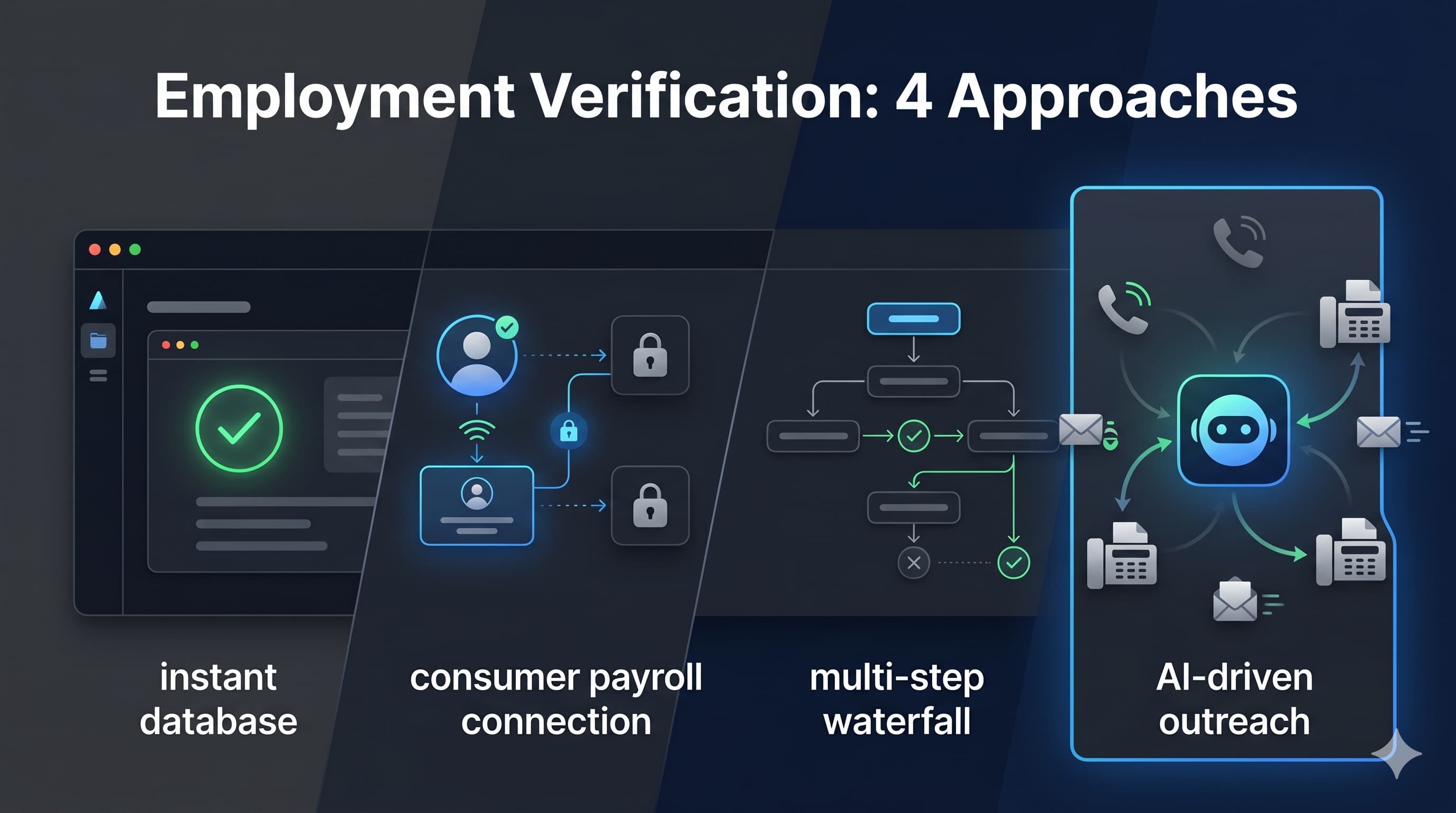

Four distinct approaches now compete for verification volume: consumer-permissioned payroll connections (Argyle), multi-method waterfall with human fallback (Truework), employer-contributed database lookup (The Work Number), and AI-powered verbal outreach (Superunit). Each solves a different part of the problem. No single tool covers every employer type. The right choice depends on your use case, employer mix, and tolerance for coverage gaps. For a broader look at the provider landscape, see our breakdown of the best employment verification platforms for 2026.

Why Verification Method Selection Has Direct Cost Implications

Choosing the wrong verification tool shows up fast: coverage gaps on small employers, failed verifications that stall mortgage closings, per-report costs that compound across thousands of monthly requests. The Work Number's January 2026 price increase made cost-per-verification a first-order budget concern for teams that had been on autopilot with Equifax for years.

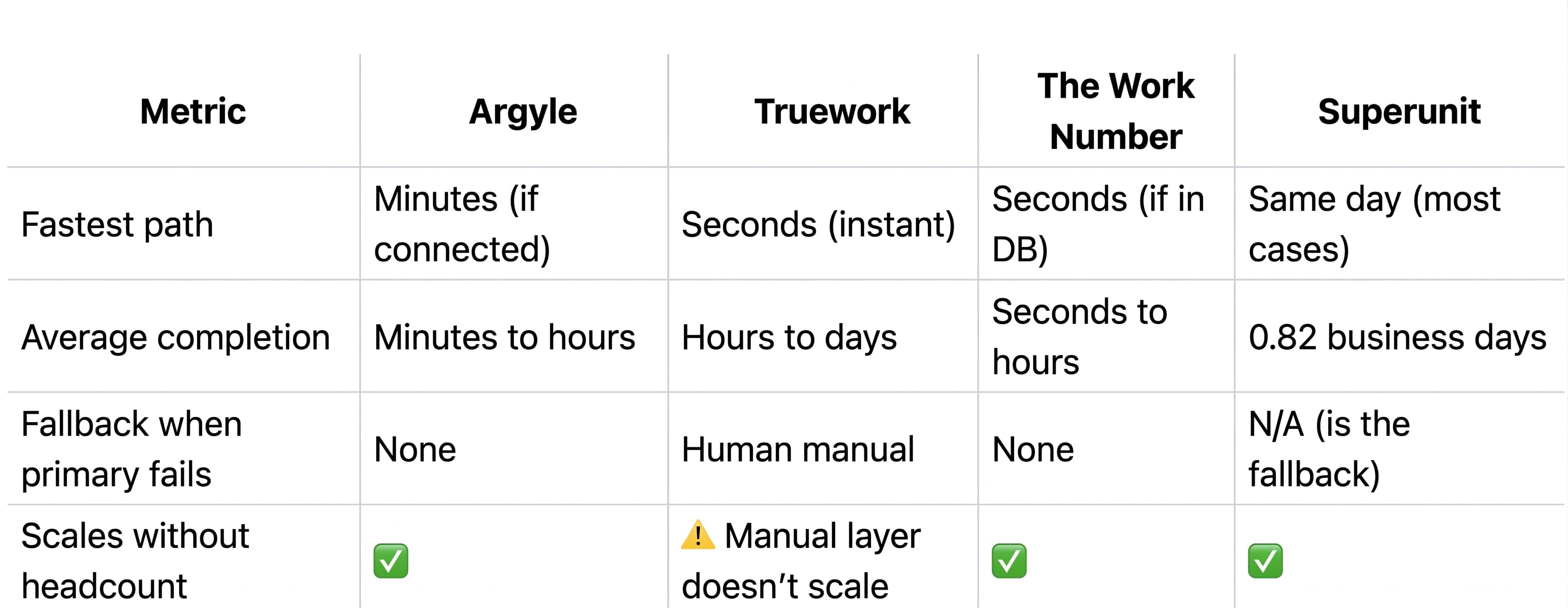

Database solutions (TWN) and consumer-permissioned tools (Argyle) both fail when the employer isn't in the database or the applicant won't connect their payroll account. When those methods miss, someone has to pick up the phone. That "someone" has traditionally been a manual verification team. Slow, expensive, and hard to scale.

Snapshot: Four Approaches Compared

How We Evaluated These Four Platforms

Each vendor was assessed across seven dimensions: data source model and employer coverage, verification method (instant vs. consumer-permissioned vs. verbal outreach), API and integration capabilities, pricing model and cost per verification, turnaround time and completion rate, vertical use case fit, and compliance documentation. The goal was to identify which tool fits which workflow, not to declare a universal winner.

Data Sources and Employer Coverage

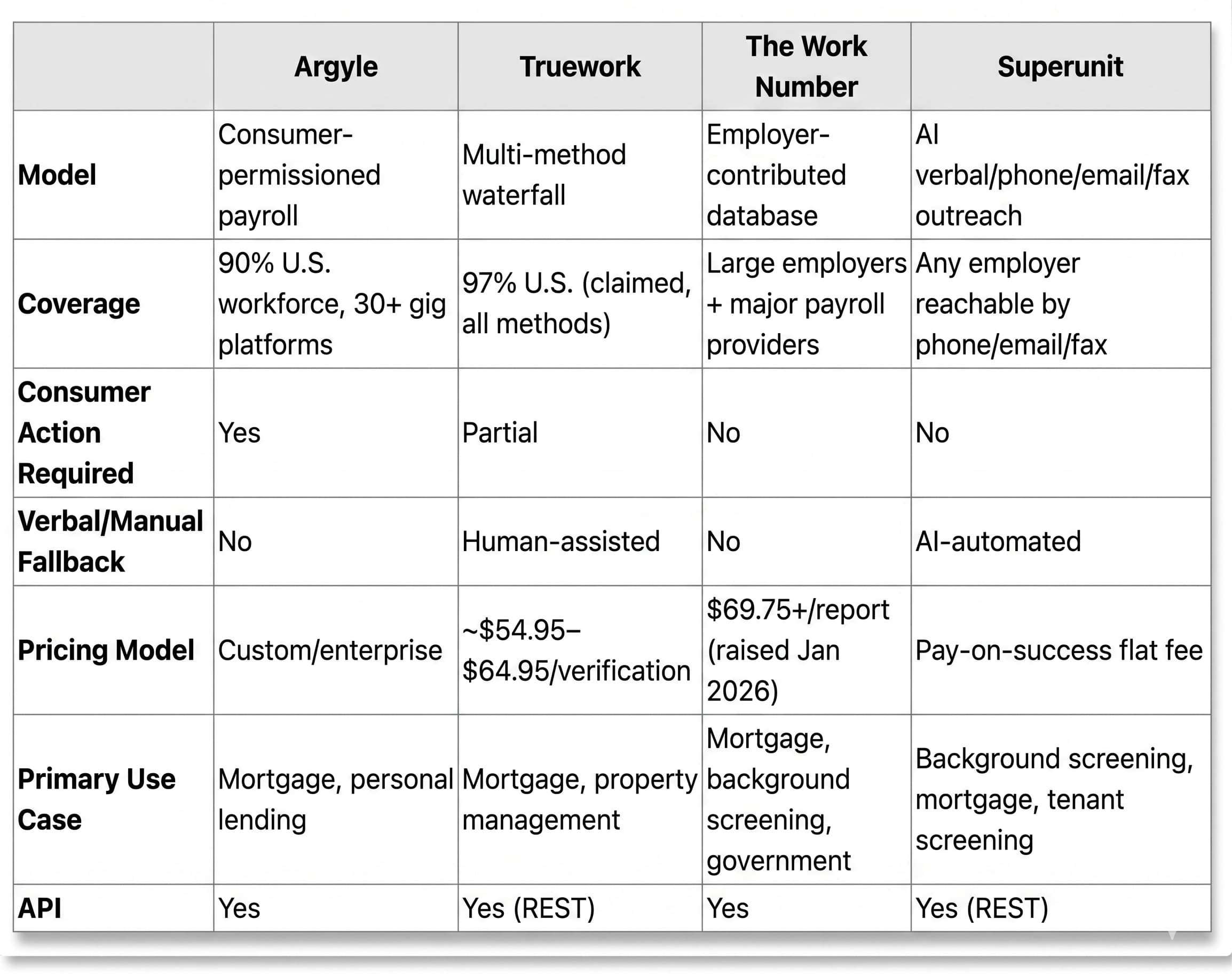

Argyle

Best for: Mortgage lenders and consumer lenders with digital-first borrower workflows where the applicant will connect their payroll account.

Pros:

- 90% U.S. workforce coverage (per Argyle's published figures) through direct-source payroll connections, including 30+ gig platforms and 170+ data points per connected record

- Self-employed and gig worker support via platform integrations that database solutions miss entirely

- 90%+ data completeness on connected records, pulling job titles, start dates, wages, deductions, and commissions from payroll systems directly

Cons:

- Argyle requires the consumer to connect their payroll account. The 55%+ VOIE conversion rate means roughly half of applicants never complete the connection, creating a coverage ceiling that no amount of UX optimization fully solves.

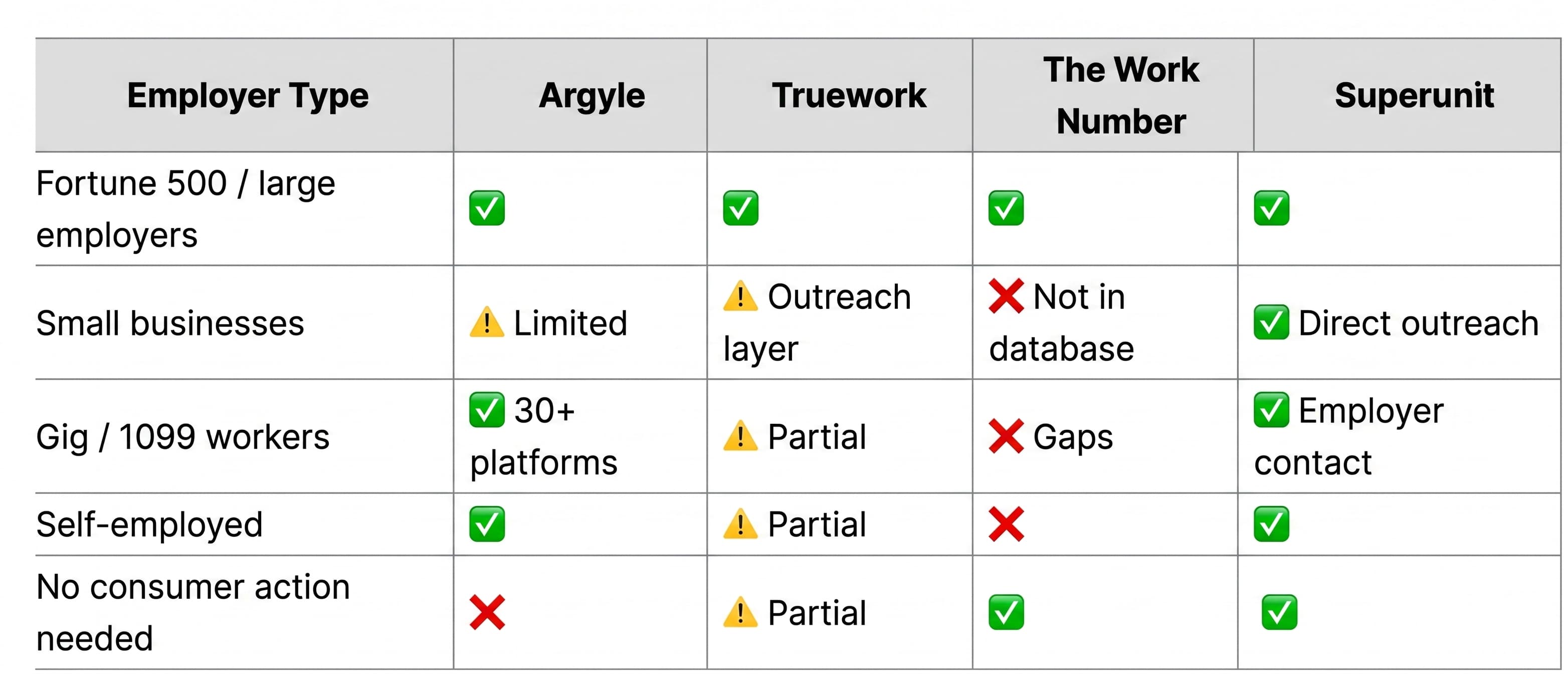

- No verbal outreach capability. When a consumer won't or can't connect, you need a separate vendor.

- Small employer coverage depends on whether the employer uses a supported payroll platform. Mom-and-pop shops running payroll through QuickBooks Desktop or paper checks are effectively invisible.

Truework

Best for: Mortgage lenders and property managers who want a single platform spanning instant database hits, automated outreach, and human manual fallback.

Pros:

- Multi-method waterfall moves from instant database lookup to smart outreach to human-assisted manual verification, claiming 97% U.S. coverage across all layers combined

- Transparent published pricing at $59.95 for VOE, $64.95 for VOI, and $19.95 for reverification

- Mortgage LOS integrations with Encompass, Empower, Blend, and nCino reduce workflow friction for lender teams

Cons:

- The manual fallback layer runs on human effort. Scaling verification volume means scaling headcount, and turnaround times stretch when the team is busy.

- Hard-to-reach employers (a restaurant that only answers the phone during off-peak hours) still depend entirely on a human rep getting through. No AI automation on the outbound call side.

- That 97% coverage figure combines all methods, including the slowest and most expensive manual layer. Real-world speed and cost vary significantly depending on which layer does the work.

The Work Number (Equifax)

Best for: High-volume teams verifying employment at large enterprises and major payroll providers where database hit rates are consistently high.

Pros:

- Instant results in seconds for employers who contribute payroll data to the Equifax database, built over 30+ years

- Encompass and federal integrations including Tyler Technologies and GSA make TWN a standard in mortgage and government workflows

- No consumer action required, since employers contribute data directly to Equifax

Cons:

- The January 2026 price increase raised already-high costs. Reports start at $69.75 and have historically reached $130.69 for certain use cases. Equifax sets the pricing, and pass-through vendors have limited negotiation leverage.

- When an employer isn't in the database, TWN returns nothing. No outreach, no fallback. Small businesses, gig workers, and self-employed individuals produce a dead end.

- Budget predictability is limited because Equifax controls the rate schedule. Teams that built their unit economics around $69.75 reports are now recalculating.

Superunit

Best for: Background screening companies, mortgage lenders needing verbal VOE fallback, and tenant screeners verifying applicants at small or hard-to-reach employers.

Superunit deploys AI voice agents that call HR departments and employer contacts via phone, email, and fax simultaneously. No database, no consumer permission. The contact research layer draws from approximately 100 million business records worldwide, so coverage extends to any employer with a working phone number, email address, or fax line.

The operational shift is concrete: what used to take a dedicated staffer an entire morning (calling, waiting on hold, leaving voicemails, calling back) gets compressed into parallel automated attempts across channels.

Pros:

- No consumer permission required, which fits background screening workflows where the screener initiates the verification

- 0.82 business day average completion with 65% of verifications finished within 24 hours and 80% within 48 hours, based on 70,000+ verifications across 45 customers

- Pay-on-success pricing with a flat fee for successful verifications; failed or unable-to-verify outcomes cost nothing, and a free tier is available for testing with no minimum volume commitments

- Full audit trail on every case with recorded and transcribed calls, timestamps on all contact attempts, and documented pass/fail/unable-to-verify outcomes that support FCRA compliance and adverse action documentation

- Scales without adding headcount, with AI agents handling simultaneous outbound attempts across channels

- Covers small employers and hard-to-verify cases that database solutions structurally cannot reach

Cons:

- 66% overall completion rate. That means 34% of verifications don't reach a confirmed result. Most failures trace to employers who simply don't respond across any channel. Manual teams hit the same wall, but the number matters: if you submit 1,000 verifications, expect roughly 340 to come back unable-to-verify.

- No native mortgage LOS integration (Encompass, Blend, etc.). Integration is via REST API, which requires development effort. Argyle and Truework have pre-built connectors that Superunit lacks.

- Founded in 2024 (YC S24 batch). Less operational history than any competitor on this list. The 70,000+ verification volume across 45 customers provides a performance baseline, but that's a fraction of what TWN or Truework have processed.

A background screening customer case study shows the typical operating profile: 62% completion rate with sub-1-day average turnaround, replacing manual phone verification workflows that previously required dedicated staff.

Employer Coverage by Type

Turnaround Time and Completion

Instant tools are faster when they hit, but they produce dead ends when the employer isn't covered. Superunit is slower than a database lookup (hours vs. seconds) but covers the cases where databases return nothing. Most teams running high volumes end up needing both layers.

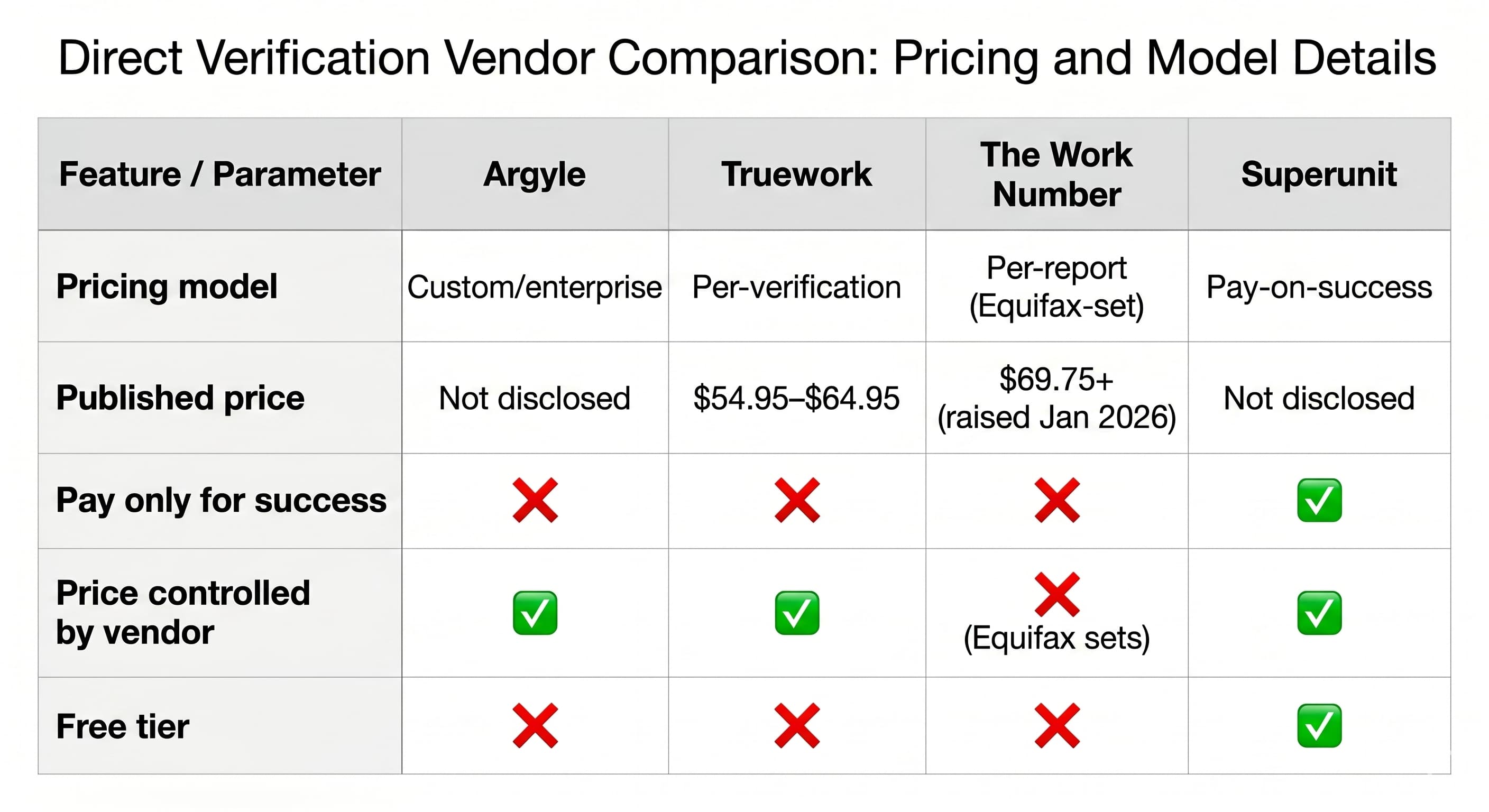

Pricing Comparison

The pay-on-success model is a structural difference. Argyle, Truework, and TWN all charge per request or per report regardless of outcome. With Superunit, if the verification doesn't complete, you pay nothing. For teams with high volumes of hard-to-verify employers (small businesses, informal employment), cost savings compound since you're only paying for the roughly 62% that succeed. The flip side: Superunit doesn't publish pricing, so you can't model costs until you get a quote.

Use Case Fit by Vertical

Mortgage

Argyle and Truework both have strong mortgage LOS integrations (Encompass, Blend, nCino). Argyle's Day 1 Certainty-compatible workflows and PBSA accreditation make it particularly attractive for GSE-aligned verification scenarios. The Work Number remains the default for large-employer borrowers where instant speed is the priority. For a detailed comparison of mortgage employment verification providers and VOE/VOI options, we break down the differences by lender workflow type.

Superunit fits mortgage as a verbal VOE fallback for mortgage lenders. When TWN returns no result and the borrower won't connect via Argyle, Superunit's AI agents can call the employer directly for pre-closing verification. The 0.82 business day turnaround keeps most closing timelines intact. The missing LOS integrations mean your team needs to build the API connection, which adds implementation time.

Background Screening (CRAs)

Argyle requires consumer permission, which doesn't match the standard CRA workflow where the screener initiates the verification. TWN is the incumbent, but the January 2026 price increase is driving active re-evaluation across the industry.

Superunit fits the CRA workflow without requiring consumer action and scales without adding verification staff. Every call is recorded for compliance documentation. The 62% completion rate from background screening customer data means you'll still need a process for the 38% that don't complete. That incomplete rate is comparable to what manual teams see on the same hard-to-reach employers, but it's not zero.

Tenant Screening

Tenant applicants frequently work at small businesses that aren't in TWN's database and don't use payroll platforms that Argyle connects to. Truework's outreach layer can help, but the human-assisted fallback adds cost that's hard to justify at rental verification price points.

Superunit's same-day verbal VOE for tenant screening, combined with offer letter verification, covers the typical tenant screening scenario where you need fast confirmation from a small employer.

Who Each Platform Serves Best

Argyle: Digital-first mortgage lenders whose borrowers will connect payroll accounts. Teams needing GSE-aligned or Day 1 Certainty-compatible VOI workflows. Lenders looking to replace TWN for borrowers at large employers who use supported payroll platforms.

Truework: Mortgage lenders and property managers who want one platform across instant, outreach, and manual verification layers. Teams already integrated with Encompass, Blend, or nCino who want transparent per-verification pricing.

The Work Number: Large-employer-heavy workflows where database hit rates stay above 80%. Government agencies and regulated lenders with established Equifax relationships. Use cases where sub-second speed is the primary requirement and the employer is consistently in the database.

Superunit: Background screening companies needing verbal VOE without consumer permission. Mortgage lenders who need a fallback when TWN, Argyle, or Truework return no result. Tenant screeners verifying applicants at small employers. Teams replacing manual verification staff with automation, provided they can absorb a ~34% unable-to-verify rate.

Frequently Asked Questions

What happens when The Work Number returns no result? TWN has no built-in fallback, so the verification simply fails. Truework's smart outreach layer can attempt employer contact. Superunit's AI agents call the employer directly via phone, email, and fax.

Do I need the applicant's permission to use these tools? Argyle requires the consumer to connect their payroll account. The Work Number and Superunit do not require consumer action. Truework's instant layer doesn't require consumer action, but some methods in the waterfall may.

How do these tools handle small business employers? The Work Number has significant gaps for small employers not in the database. Argyle covers them only if the employer uses a supported payroll platform. Superunit contacts any employer directly, regardless of size or payroll provider.

Which tool works best for background screening companies? Superunit requires no consumer permission and scales without headcount. TWN is common but expensive, especially after the January 2026 price increase. Argyle's consumer-permissioned model doesn't fit the standard CRA workflow.

Which tools integrate with mortgage LOS platforms? Argyle integrates with Encompass, Byte, Vesta, nCino, Empower, and Blend. Truework integrates with Encompass, Empower, Blend, and nCino. The Work Number connects to Encompass. Superunit offers REST API integration but no pre-built LOS connectors.

Final Verdict

No single vendor covers every scenario. Argyle and TWN are fastest when they hit. Truework offers the broadest single-platform coverage. Superunit fills the gap that all three leave open (employers not in a database, consumers who won't connect payroll), but it's slower than instant methods and its 66% completion rate means a third of cases won't resolve.

The practical answer for most high-volume teams: use a database or consumer-permissioned tool as the first pass, then route failures to verbal verification. If you're currently staffing that verbal layer with humans, Superunit replaces the headcount. If you're just skipping those verifications entirely, Superunit picks up volume you're leaving on the table.

Superunit's free tier requires no minimums if you want to test it against your actual case mix.

Ready to get started?

Major CRAs trust us to handle the verifications no one enjoys — faster, cheaper, and fully documented. See how!